Monopoly

A monopoly

A market where one firm dominates the market for a good that has no substitutes and where significant barriers to entry exist.

- There is only one seller (price maker)

- The product is unique, there are no substitutes

- There are very high barriers to entry into and exit (high setting up cost) from the market

- Firms outside the market will lack perfect information

Barriers to entry

A range of obstacles that deter or prevent new firms from entering a market to compete with existing firms. (so, there is no difference between short-run and long-run)

- High fixed cost or setup cost

- Advertising and brand names with a high degree of consumer loyalty

- Economic of scale

- Patent

- The pace of product innovation

- Collaboration between existing producers to develop new products may act as a barrier

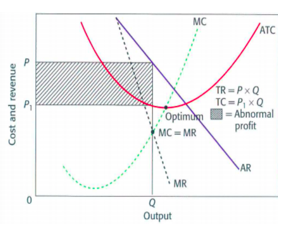

- Profit-maximising monopolist would choose the output where MC = MR.

- If the total revenue is higher than the production costs, it will make abnormal profit. This will be a permanent feature.

- In monopoly, there is no distinction between the short run and the long run because of the barriers that prevent the entry of competitors.

- There is no economic incentive for the monopolist to move away from the profit-maximizing output Q

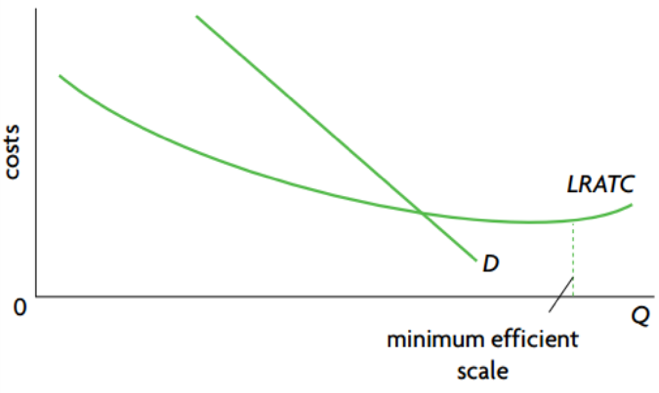

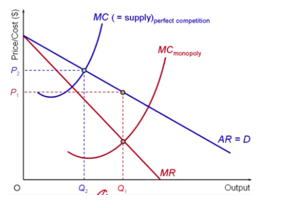

Natural monopoly

A firm that has economies of scale so large that it is possible for the single firm alone to supply the entire market at a lower average cost than two or more firms. It occurs in a market where the lowest costs can be achieved when only one firm sells to the market. It is typically associated with large fixed start-up costs.

If the market demand for a product is within the range of falling LRATC, this means that a single large firm can produce for the entire market at a lower average total cost than two or more smaller firms. When this occurs, the firm is called a natural monopoly.

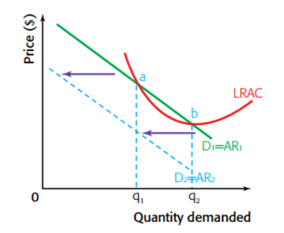

If new firm B enter the market, the market demand will be divided by firm A and B. Thus, the demand curve for firm A will be shifted leftward.

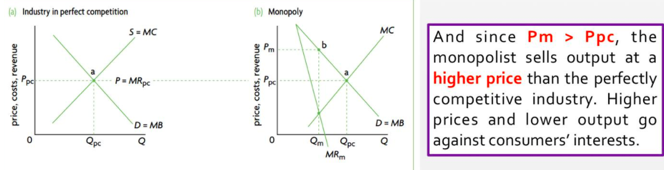

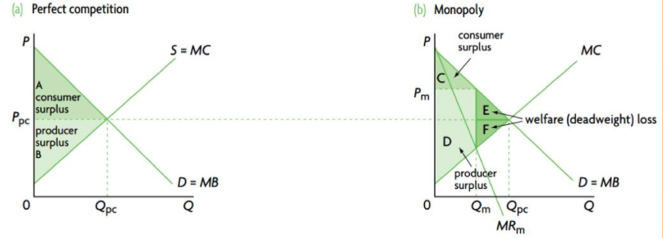

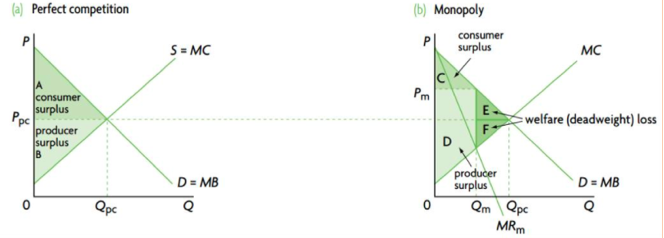

Outcomes of monopoly

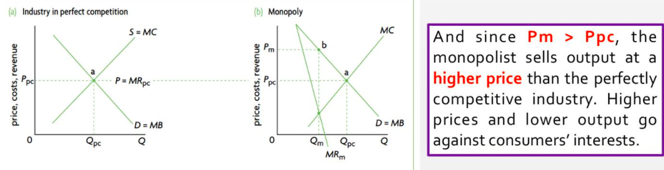

- Higher price and lower output

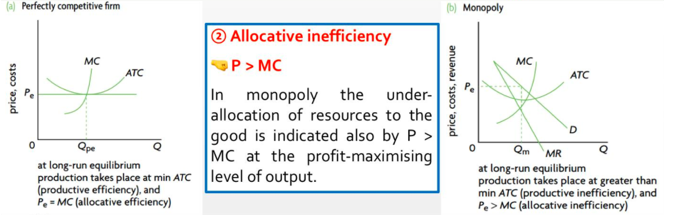

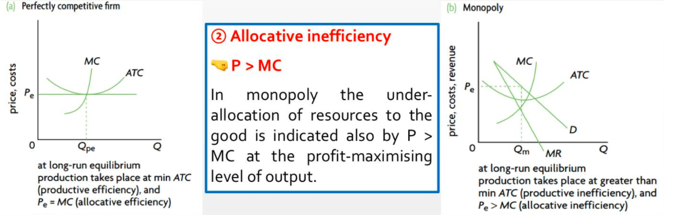

- Allocative inefficiency (MC is not equal to AR, loss of consumer and producer surplus)

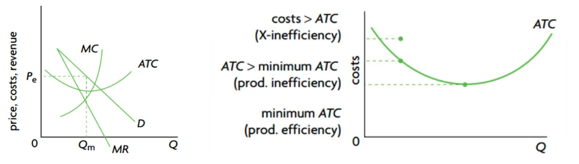

- Productive inefficiency (production at higher than minimum ATC)

a. Lack of competition in monopoly may lead to higher cost (X-inefficiency: producing at higher than necessary ATC) due to poor management, a poorly motivated workforce, lack of innovation and use of new technologies.

Policies:

-

Legislation (government can force the firm to charge a price equal to its average total cost)

-

Regulation

AD

- To promote competition by preventing collusion between oligopolistic firms.

- To manage and control mergers

- To ensure more socially desirable price and quantity outcomes

DIS

- The laws themselves may be vague, allowing much room for different interpretations

- Laws in particular country may be enforced to varying degrees.

- It is difficult to discover evidence of the collusion and to prove it

-

Nationalization (State ownership)

-

Trade liberalization (introduce foreign competitors)

-

Privatization (Encourage competition)

Situations which government should NOT control the monopoly power

- Natural monopolies (some are state-owned & do not aim to maximize profit)

- Ability to achieve economies of scale may lead to lower unit cost and price than a competitive industry

- Monopoly profits as a source of funds for investment / research & development

- They need to keep innovating to maintain economic profit

- Protect intellectual property right

- Protection of strategic industries against foreign competition

- Provision of otherwise profitable goods through price discrimination

Situations which government should control the monopoly power

- Abuse of monopoly power: higher price and lower output

- Less choice for consumers

- Abnormal profits are not justified

- Lack of competition: leads to lower incentive to improve & to innovate

- Allocative & productive inefficiency & misallocation of resources

Evaluation of monopoly compare to perfect competition market

Advantages:

- Ability to finance R&D

- Possibility of substantial Eos

Disadvantages:

- Higher price & lower output

- Lack of allocative & productive efficiency

- Lack of competition

No Comments